Robinhood Chain's First Week: $100M in TVL, and Most of It Isn't the Meme Coin

Two different metrics tell two different stories. Most coverage only reports one of them.

Robinhood Chain crossed $100 million in total value locked within its first seven days of operation. That number is real, verified across independent data sources, and worth taking seriously. What most coverage got wrong in the first 48 hours - including an earlier version of this article - is what that number is actually made of.

TVL and DEX volume measure two different things, and on Robinhood Chain they tell two different stories. Roughly $90 million of the $100 million in locked capital sits in Morpho, an on-chain lending protocol integrated at launch - money seeking yield, not meme exposure. The meme coin driving the headlines, CASHCAT, shows up almost entirely in trading volume, not in TVL. Conflate the two and you get a headline that's directionally wrong about what's actually durable here.

What Robinhood Chain Actually Is

Robinhood Chain is a permissionless Ethereum Layer 2 network built on the Arbitrum stack, running 100ms block times, which launched to public mainnet on July 1, 2026, following a public testnet that ran from February. It settles to Ethereum for security and uses ETH as its native gas token - every transaction on the network, regardless of what's being traded, requires ETH to execute, and there is no separate Robinhood-native token.

The chain shipped with real infrastructure partners on day one: Uniswap for spot trading, Chainlink for price oracles, and Morpho for lending. This wasn't an empty chain waiting for an ecosystem - it launched with one, and that lending integration turned out to matter more than the trading venue. The speed of that ecosystem forming is a textbook case of network effects — liquidity attracts liquidity.

Critically, the chain is permissionless: Robinhood operates the infrastructure but cannot prevent third parties from deploying tokens or smart contracts on top of it. That single design choice is the structural reason a meme coin was able to dominate the network's first week independent of anything on Robinhood's own roadmap.

The stated purpose is tokenized real-world assets: Stock Tokens, available through Robinhood Wallet in more than 120 countries (availability varies by jurisdiction), designed to let users trade tokenized equities around the clock and use them as DeFi collateral.

Two Numbers, Two Different Stories

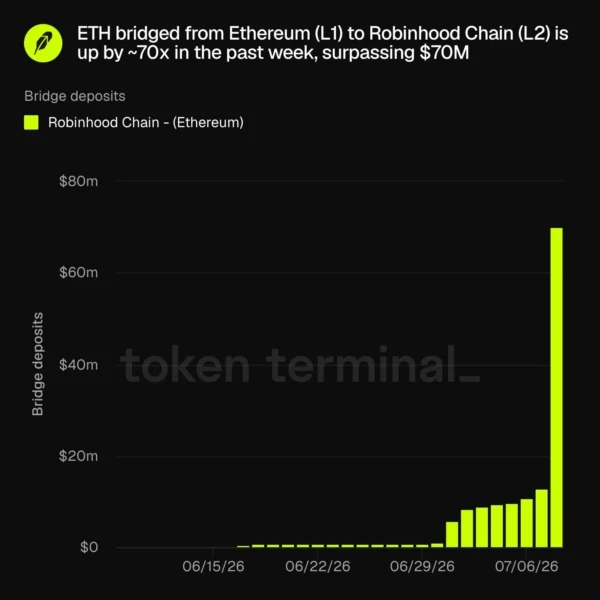

TVL climbed from $39 million on day three to $50 million on day four to roughly $100 million by the end of week one. About $90 million of that sits in Morpho lending pools. Lending capital is structurally stickier than trading volume - users depositing into a lending protocol are seeking ongoing yield, not executing a trade and leaving. That's a meaningfully different signal than a wallet briefly holding a meme coin.

ETH bridging volume as of July 9-10, before the week-one TVL total reached $100M. Source: Token Terminal.

DEX volume tells the speculative story. On July 8, Robinhood Chain posted between $560-570 million in 24-hour DEX volume, briefly overtaking Hyperliquid as the largest decentralized exchange by that metric. The catalyst was CASHCAT, a meme coin trading on Uniswap WETH pairs that hit an all-time high above $0.14 and briefly reached a $100-150 million market cap. CASHCAT alone accounted for roughly $98 million of that single day's volume.

Daily active addresses approached 200,000 at peak, with more than 140,000 first-time users in a single day. Over 13,900 smart contracts were deployed in the first week - a figure that reflects the permissionless design as much as genuine developer interest.

The Number Nobody's Explaining

140,000+ new wallets in a day is a genuinely large spike for a network one week old. The obvious read - and the one most coverage implicitly encourages - is that it reflects broad interest in Robinhood's tokenization vision.

The wallet surge coincided almost exactly with CASHCAT's breakout, a meme coin referencing Robinhood's early "Cash Cat" mascot. Uniswap pool volume and active address charts both show a sharp inflection starting July 7-8, directly aligned with the token's rise, not with any RWA product milestone.

Robinhood CEO Vlad Tenev acknowledged the dynamic directly on X on July 8, noting the chain was built for real-world assets but "works great for memes too." One trader reportedly turned roughly $85 into over $2 million holding CASHCAT through the run-up - the signature pattern of speculative token-launch activity, not institutional or retail RWA adoption.

This is a familiar sequence in new blockchain launches, and a recurring test of market efficiency — how fast speculative premia get arbitraged away. Solana's early growth followed a similar path: meme-driven liquidity arrives first, serious applications arrive later, if they arrive at all. Analysts drawing that comparison aren't being cynical - it's the standard playbook for bootstrapping a new chain's liquidity, and Robinhood's enormous retail distribution just executed it faster than most. Notably, by the end of week one, DEX volume had already normalized down into the tens of millions per day - the expected pattern after any speculative spike, and faster than most chains take to come back down.

There's a cost to that openness, too: within the same week, scam reports tied to the network's rapid token proliferation began surfacing, the predictable downside of a permissionless chain that lets anyone deploy anything.

The Part That Should Concern Actual Investors

Buried in Robinhood's own disclosures is a structural detail that matters more than the wallet count: Stock Tokens are not stock. They are tokenized debt securities issued by a Robinhood subsidiary — Robinhood Assets (Jersey) Limited — that track the underlying stock's price but confer no legal or beneficial ownership in the security itself.

This isn't a new controversy. It drew scrutiny when Robinhood first issued tokenized shares of OpenAI and SpaceX to EU customers, prompting OpenAI to publicly clarify it had not endorsed or been involved in the offering. The structure lets Robinhood offer price exposure to equities — including private companies that don't trade on public markets — without the regulatory overhead of an actual securities offering. For a platform serving nearly 28 million customers across three continents, that's a meaningful distinction to bury in the fine print.

None of this means Stock Tokens are illegitimate. Price-tracking derivative structures are common and legal. It means the "tokenized stocks" framing in most coverage — including the framing implicit in describing this as bringing "traditional financial assets... together on a single blockchain platform" — overstates what's actually being offered.

Why This Still Matters for Ethereum

Whatever is driving each individual metric - lending yield or meme speculation - the mechanism benefits Ethereum identically, because Robinhood Chain uses ETH as its gas token by design rather than a Robinhood-native token.

HashKey Group researcher Tim Sun made this point plainly: the direct benefit to Ethereum isn't which application drives usage, it's that any usage at all requires ETH. As bridged assets, wallet addresses, and on-chain transactions grow, that growth is structurally, mechanically tied to ETH demand - independent of whether the growth comes from lending deposits, tokenized shares, or a meme coin named after a mascot.

This is the same dynamic that made Arbitrum and Optimism valuable to Ethereum's broader thesis, and it's fundamentally a question of platform economics: Layer 2 activity, whatever form it takes, ultimately settles back to and depends on the base layer that captures the value. Robinhood didn't need to build a "good" chain by RWA standards to make this true. It needed to build a chain people actually use, and route the gas costs through ETH. It did both in a week.

What Actually Determines Whether This Lasts

The uncomfortable truth about meme-coin-driven launches: the incentive structure that generates the first wave of trading activity is usually the same structure that kills it. Speculative token launches attract capital fast and lose it just as fast once the next opportunity emerges elsewhere - and DEX volume had already normalized to the tens of millions per day by the end of week one, well ahead of the usual timeline.

The lending side is the more interesting long-term signal precisely because it didn't behave that way. $90 million sitting in Morpho after a week - capital that's earning yield rather than chasing a pump - is the closer proxy for whether Robinhood's actual thesis (bring brokerage users into on-chain finance) is working. Robinhood has one advantage most Layer 2 launches don't: a captive base of nearly 28 million existing brokerage customers who don't need to be acquired, only converted. Whether that lending TVL keeps growing after the meme cycle has fully faded, or whether it was itself partly incentive-driven and thins out too, is the number actually worth watching next. For a broader take on separating durable value from hype in this market, see why free AI models are an investment thesis.

The Bottom Line

The $100 million TVL figure is real, and the underlying mechanism - ETH as gas, a real lending integration at launch, a captive retail base - is a legitimate structural advantage most new L2s don't have. But the composition of that number matters more than its size. Roughly 90% of locked capital sits in a lending protocol seeking yield, not in the meme coin generating the headlines - and the meme coin's trading volume, which did dominate the news cycle, has already cooled within the first week.

That doesn't make the launch a failure, and it doesn't make it a triumph of the tokenization thesis either. It makes the first week what most first weeks are: a liquidity bootstrap with two distinct signals running in parallel, only one of which is likely to still be here in three months. The number worth tracking from here isn't this week's TVL total - it's whether the Morpho lending balance keeps growing after the CASHCAT cycle is fully spent, and whether Stock Token volume - the actual RWA product - ever becomes large enough to matter next to either of them.

For the wider debate over whether crypto assets hold durable value or trade mostly on narrative, see Bitcoin vs. gold: can they be compared? — the same signal-versus-speculation question, applied to the asset class itself rather than a single chain launch.

What is Robinhood Chain built on?+

Robinhood Chain is a permissionless Ethereum Layer 2 network built on the Arbitrum stack, running 100ms block times. It settles to Ethereum for security and uses ETH as its native gas token, with no proprietary Robinhood token.

Do Robinhood Stock Tokens give you ownership of the actual stock?+

No. Stock Tokens are tokenized debt securities issued by Robinhood Assets (Jersey) Limited that track the underlying stock's price. They do not confer legal or beneficial ownership in the security itself - a structure that drew scrutiny when Robinhood first launched tokenized OpenAI and SpaceX shares in the EU.

Is Robinhood Chain's TVL mostly from meme coin speculation?+

No. Of the roughly $100M in TVL after week one, about $90M sits in Morpho, an on-chain lending protocol integrated at launch. The meme coin, CASHCAT, drove trading volume, not locked capital - those are different metrics and got conflated in a lot of early coverage.

Why did meme coins take over Robinhood Chain so quickly?+

The chain is permissionless: Robinhood controls the infrastructure but can't prevent third parties from deploying tokens or smart contracts on top of it. That openness is what let CASHCAT and thousands of other tokens launch within days, independent of Robinhood's own product roadmap.